Relentless Rate Hikes Punish Markets

October 24, 2022

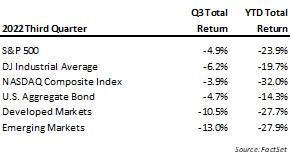

The third quarter saw no relief from the pressure financial assets have faced all year and marked the third straight quarter of declines for both stocks and bonds. Foreign markets generally did worse, pressured by the relative strength of the U.S. Dollar and the fallout from the European energy crisis. 2022 continues to set many milestones with the unrelenting path of decline and the breadth of losses across various assets, including those that historically have offered inverse return characteristics in times of turmoil. The primary factor pressuring assets was the hawkish commentary from the Fed, coming despite the emergence of possible cautionary signals in the economy and financial system. In the third quarter, we believe the market started to ratchet up fear the Fed’s obsession with reducing inflation could come at the cost of severe economic or financial dislocation.

For perspective on returns so far in 2022, the chart below shows how various assets have performed year to date. An aggressive Fed and investors reducing risk have made the U.S. Dollar one of the few winners along with energy which has risen in response to disruptions from the war in Ukraine. Virtually everything else has been in the red with low-coupon long-maturity bonds seeing their largest decline in history. This means the standard 60/40 portfolio allocation, a strategy that has worked well for decades, is down more than 20% YTD and, per Bank of America research, seeing the worst return in 100 years. The breadth and depth of decline are partly due to the significant run many assets enjoyed post-COVID, but also a product of the speed and magnitude of change in policy rates. Coming off zero-bound targets, the relative change policy makers have dropped on the markets in the past nine months has been enormous.

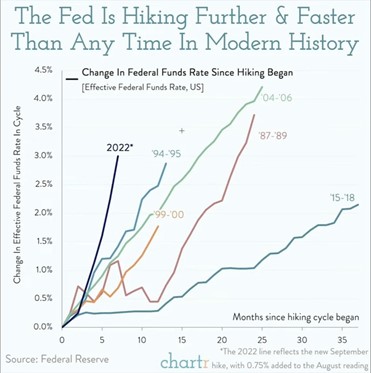

After hanging on to the “transitory” label for far too long, the Fed has now fully embraced the idea that it will solve inflationary problems through aggressive rate increases. The Fed Funds target started the year at 0%-0.25% and after eight months of action stands at 3.0%-3.25%. Current talk among Fed members is they will continue to hike until reaching a target of 4.5%-5.0% and/or inflation gets back to around 2%. As of now, the focus is quite myopic on lowering CPI and the Board has expressed little concern about the risk of collateral damage.

We think the commitment to this rather singular strategy stems from the view that past Fed Chairman Paul Volker successfully used higher rates to end the inflation pressures of the ‘70s and while there was economic fallout at the time, the end goal of crushing inflation was deemed to be worth it. However, we note the “fix” in the ‘80s came against a very different backdrop. The economy had a fraction of the outstanding private and public debt and very different trends in supply constraints. Energy, for example, was enjoying new sources of supply from Russia which worked in part to alleviate the oil cost pressures emanating from the Middle East in the ‘70s.

The practical challenge in employing monetary policy to quash inflation is that changes filter through the economy with a lag. We think it is virtually impossible to know in real time whether changes are enough or too much. Too much in a highly leveraged and integrated economy can risk “breaking something”. There is a long history of rapid changes in rates or currencies tipping off financial fallout. Modern-day examples include the ’08 housing crisis (rates), the collapse of Lehman and Bear Stearns (rates), the failure of the fund Long Term Capital Management (currencies), the tech bubble (rates), and the Orange County debt default (rates). In our opinion, a clear sign of caution came just a few weeks ago when the Bank of England had to support the price of long-term bonds to avoid default by UK pension firms. Pension firms typically hold debt securities with very long maturities, the value of which are very sensitive to changes in market rates. The leverage used by many financial firms (both in term structure and rates) may suggest other financial firms are seeing increased stress after such large and fast policy rate changes.

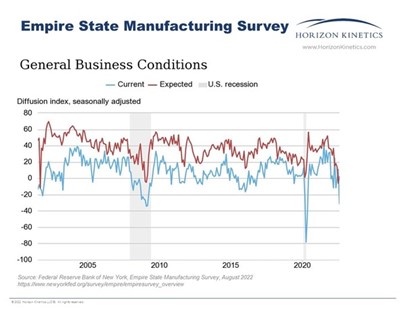

Aside from financial structure concerns, we also see a growing list of indicators the broad economy is feeling the stress of rate changes. Last quarter we noted how higher rates had impacted the housing market as elevated mortgage rates increased canceled deals, fewer transactions, and an uptick in listings cutting prices. More recently there is evidence consumer consumption and business sales activity have taken a hit on a wider scale. In September FedEx provided a very cautionary outlook on global shipment volumes and was soon followed by companies like Nike, AMD, nVidia, and Carmax issuing significant cuts to sales and profit guidance. Each of these companies pointed to a rapid softening of demand while several also reported significant inventory increases (a drag on future profits).

Media and economists have debated whether the economy is now in recession. The definition of two consecutive quarters of contracting GDP has been met, but the nuances around the COVID recovery and disruptions from the war have left some defenders. From a formal standpoint, the National Bureau of Economic Research (NBER) determines recession start and end dates after the fact, but incoming data sure makes it feel like a recession is either here, or very close. Housing is a significant part of the U.S. economy, and it has slowed significantly at every stage. Consumer consumption is showing signs of rolling over in front of the holiday season and the view from business managers also has deteriorated. Raising rates into a recession doesn’t usually happen and in our view can increase the potential severity of an economic downturn.

Many of the risks in the financial system now are directly related to the policy decisions of the past. Years of suppressed rates and stimulative programs have enticed institutional and individual investors to take on more risk. The risks can come in many forms – credit risk in lending to lower quality borrowers to achieve a yield target, investing over a longer horizon, or financing less-proven businesses in the hopes of higher reward. Like it or not, monetary policy plays a significant role in defining the playing field for financial assets. If we look at how the Fed defined conditions just a year ago they were committing to “lower rates for longer”. They also said raising rates was unlikely until 2024 and that inflation is transitory and should return to 2% in 2022. Things have changed, and financial markets have been roiled in adjusting.

Important Note: As we move into a deeper discussion below related to inflation and supply issues, we recognize that some topics can become politically charged. We are not advocating for any party or political outcome nor are we taking a stand on green energy. Our comments are based on data, research, and analysis of other countries that have embarked on similar paths and are stated with a goal of stability and success for the economy.

The key questions for the current policy approach are: will it significantly lower inflation and will it be worth the costs (recession, higher unemployment)? Given the factors driving inflation, we think it is unlikely the Fed will be able to achieve the magnitude of inflation reduction desired without a significant amount of economic pain. In the extreme, it would be like burning down your house to solve an infestation – hardly a successful way to deal with the problem. Aggressively hiking rates will cool consumption and investment demand (exhibit A, housing) but doesn’t address supply-side constraints. The world is still sorting through supply disruptions and shifting alliances brought about by the Ukraine war and there is not much the Fed can do to address this. Regions like Europe which had a heavy reliance on Russia for commodities/energy have experienced the worst supply and inflation shocks, though the pain of their predicament has rippled around the world. What hasn’t happened is a concerted effort to develop other reliable supplies.

In short, if supply is not adequately addressed, the Fed may not be able to effectively temper inflation.

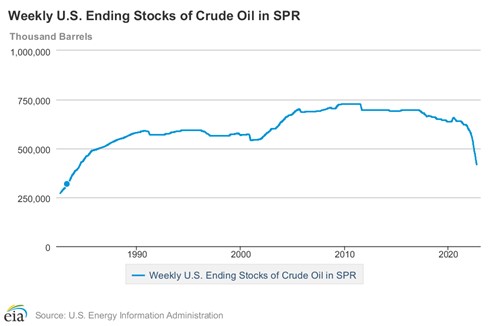

In the U.S., we are fortunate to have significant production resources internally to help offset the global energy squeeze, but long-term needs still must be considered. To this point, our efforts have been limited to quick-fix actions. Selling oil from the Strategic Petroleum Reserve (SPR) brought energy prices down this summer. While selling from the SPR was effective, this supply is finite and soon will be gone from the market. Short of a substantial reduction in demand, we expect energy prices in the U.S. to again move higher and counter efforts to reduce inflation. This is a problem that would be made even worse if there were efforts made to refill the SPR. Ideally, policy would have been using the intervening time to incentivize an increase in a reliable and friendly supply of resources but, so far, the motivation has not been there.

We believe structurally higher energy prices will be a product of the focus on building cleaner sources of energy. That tradeoff is viewed as fine by many, but we think investors must have a realistic time frame about the pace of substitution (long). Countries that have had faster adoption of green technologies still have a high dependence on traditional energy sources for many applications. Further, the fabrication of green energy technologies is itself very energy intensive and, in many steps, requires the high energy density of fossil fuels for completion. Once in place, most environmentally friendly sources of power suffer wider ranges of intermittency which means you still need a reliable baseload of supply.

In our opinion, the demand for traditional energy sources will provide investors with opportunities for years to come. This stems from both the traditional energy necessary to meet current demand as well as the supply required to implement green technologies. Additionally, commodities like copper, steel, nickel, cobalt, and lithium will also continue to see increased demand due to their necessity to meet ESG objectives. However, bringing this supply to market will likely require higher prices than seen over the past decade. Traditional fossil fuels and commodity production have been derided over the past several years and consequently seen relatively little investment. Commodities are typically a very volatile asset class, and we would expect not all commodity price changes to remain highly correlated, but we do think the next several years will require more investment in the things the world needs versus things they want (consumption goods).

Year to date, commodities have been one of the only assets to see positive returns and the strongest among these were generally the energy commodities. Other sectors have felt the pressure of compressing valuation multiples and reductions in earnings expectations as economic growth risks spread. In the second half of October, the third quarter earnings season will ramp up and investors will be assessing not only past results but management’s outlook. As previously noted, the early read from several companies has been quite negative. This has moved expectations lower, though it still may not be enough. Currently, the estimated earnings growth rate for the S&P 500 in the third quarter is 2.9%, a level that would be the lowest year-over-year growth since Q3 2020 (source: Factset). We expect most companies will have difficulty providing guidance with much confidence. The speed of rate increases is changing things rapidly and we think it will be difficult for companies to offer much confidence in their outlook.

How stocks digest softening earnings news is difficult to say after the magnitude of decline already experienced. Stock valuation based on earnings is a bit of a moving target, but the ratio is more attractive than it has been in quite some time. Using Factset estimate, the forward 12-month P/E ratio for the S&P 500 is now approaching 15x, a level below the 5-year average of 18.6x and below the 10-year average of 17.1x. Further, sentiment is now excessively bearish, and this may temper the impact of bad news. Many sentiment measures are near rock bottom, including the popular CNN Fear & Greed measure that is presently in its lowest quadrant of “extreme fear”. Likewise, statistics that capture how traders are positioned can also be good contra indicators – when markets have high short interest or lots of hedging, conditions can be right for a quick move in the other direction. Negative sentiment and oversold conditions don’t themselves trigger change but can fuel moves stemming from developments that go against that positioning (in this case, positive news). Several sentiment measures are now at or below the levels seen in March 2020 (COVID).

Ultimately, we expect a slowing economy and/or the market will force the Fed to alter its tightening policy. The slope of rate changes has had an immediate impact on demand though the full effects won’t be realized until quite a bit later. Concurrently, moving rates off a zero-bound is also clearly disrupting financial companies. In our opinion, the UK pension system news about potential insolvency should be a warning sign for other leveraged financial models, and identifying all counter-party risks preemptively is very difficult. We hope the Fed will be attuned to the risks brewing and not be forced to act in response to crisis as they have in the past.

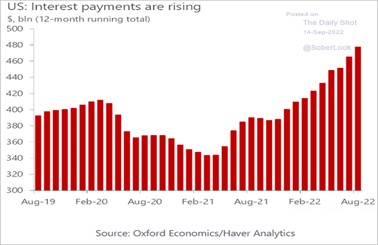

Either way, the expanding interest expense obligation of the Federal government could push the Fed to alter its course. U.S. total Federal debt of $31 billion is many times the level of the Paul Volker era and rising interest expense is quickly becoming a more significant government spending line item. With the Federal budget running deficits and not expected to change any time soon, this rising interest expense can result in a spiral that would have further negative implications for the economy and likely the value of the U.S. dollar. We don’t think the Fed can ignore this forever in considering rate policy.

Our strategy this year has been defensive due to geographic risk, interest rate risk, and growth risk. There are several areas of market risk we were able to proactively avoid, though there have been few safe havens that offered positive returns YTD. The defensive positioning includes cash balances that are at the highest we have had in years. Moving from there, this year has also seen us make direct purchases of Treasuries in several strategies which have historically been very rare. These bonds are generally in the two-year maturity window and can either be held to maturity or if conditions change enough, liquidated fairly easily. These bonds offer a little better return than cash with minimal rate or credit risk. Absent significant changes, we would expect to continue this strategy for navigating a bear market. The good news for the higher cash balances is that the Fed hiking rates has been reflected much better in our Fidelity cash sweep accounts than any of the bank account references we have checked. Not the most fulfilling news, but the objective is to protect capital during bear markets. Bear markets are usually much shorter in duration and we are well into the current one.

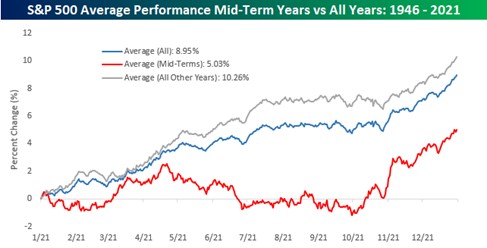

We don’t know when the next market cycle may begin or what the catalyst might be, however, our intention at this point is not to try to call the bottom. Our philosophy prioritizes the preservation of capital over trying to time the exact market bottom which elevates risk. Markets have gone through many cycles in the past and the pain of bear markets is what creates the opportunities for the next bull cycle. A possible catalyst may exist in the upcoming elections. In the past, the stock market has performed well coming out of mid-cycle elections. The chart below of mid-term election years shows a tendency for returns to be back-end loaded. Overcoming the multitude of headwinds this year is a tall order, but we will be on the lookout for change. Constructive developments in geopolitical relations or material investments aimed at alleviating supply constraints could go a long way in reducing investor nervousness.

The policy initiatives to address inflation through higher rates is a shift that most now agree came far too late. However, in playing catch up we think there are now substantial risks in going too far and too fast. Two wrongs won’t make a right. Inflation forces certainly need to be addressed, but not at the cost of badly damaging the economy. In our opinion, we are quickly approaching a time when it would be prudent for the Fed to step back and assess the effects of rate increases so far. We believe the difference in approach will be a big factor in determining the severity of this bear market and economic slowdown. As these developments unfold, we will continue to communicate any changes in our view and corresponding implications for client allocations.

While much of the focus of this update has been on the challenges the market and economy are facing, we want to take a moment to remind everyone that out of challenges come opportunities. Though we are generally positioned more conservatively, we believe opportunities will come, especially for long-term investors and our team will continue to evaluate strategies to best help you achieve your goals and objectives. We retain a sense of optimism despite the difficult period we are in.

We thank you for your continued trust in us and hope you and your family remain in good health.

Bradley Williams, Chief Investment Officer

Lowe Wealth Advisors

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Lowe Wealth Advisors, LLC), or any non-investment related content, referred to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Lowe Wealth Advisors, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Lowe Wealth Advisors, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Lowe Wealth Advisors, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are a Lowe Wealth Advisors, LLC client, please remember to contact Lowe Wealth Advisors, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives to review/evaluating/revising our previous recommendations and/or services.