By Bradley Williams, Lowe Wealth Advisors Chief Investment Officer

Precious metals can be a potential defense against currency devaluation and offer possible protection

against currency wars. Currency wars are effectively part of the end‐game that central banks

promulgate through quantitative easing. The quantitative easing is meant to stimulate growth by

lowering interest rates, creating additional money and driving more economic activity, but the

stimulative actions frequently involve the loss in global purchasing power for the currency.

Currency wars can follow because these actions do not occur in a vacuum and can have a significant

impact on global trade. After a short period, those left with a “strong” currency feel compelled to

respond in an effort to protect the export competitiveness of their own interests. The strengthening of

the U.S. dollar over the past six months is now generating more concern from businesses feeling the

impact on international trade. This will make it more challenging for our Fed to raise rates later this

year. We expect relative currency valuation issues to become a more frequent financial topic as most

central banks remain on a path of expanding their balance sheet, a.k.a. quantitative easing.

While gold doesn’t generate sales like Apple or pay a dividend like P&G, its financial role is more one of

a currency and a store of value. Gold has been recognized as a means of exchange for over two

thousand years and has historically outperformed all paper‐based alternatives in retaining value. (Past

performance is not predictive of future results)(Source FactSet). Sometimes it is more attractive than

others to hold relative to paper currencies and we believe now is likely one of those times.

We believe one way to measure the relative alternatives is to look at the cost of carry. As interests rates

continue to fall worldwide and in some cases even become negative, that lack of dividend becomes less

concerning of an issue. The alternative of holding a paper‐based currency that pays little or no interest

(and may even be negative) loses some attractiveness if there is also concern about the purchasing

power of that money sometime in the future. Interest rates on government debt with maturities

between three and five years are now negative in eight countries, while Switzerland has negative rates

all the way through their 10‐year maturity. We believe this increases Gold’s relative attractiveness as an

asset.

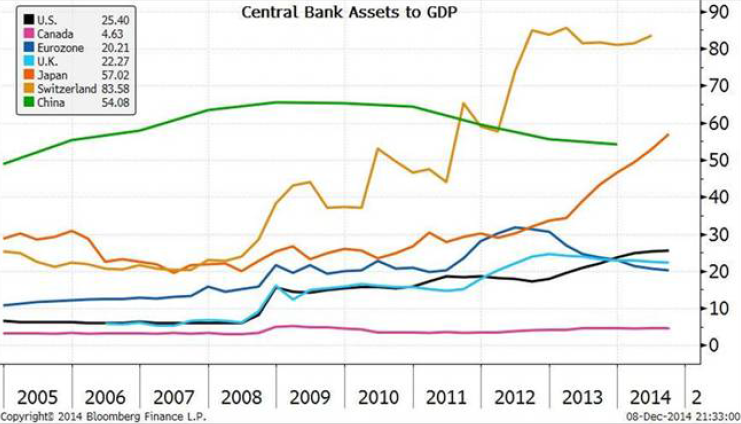

Central bank policies in the U.S. and U.K. have coincided with improvements in the respective

economies, although as a result of substantial investment for which the true return is still difficult to

measure. The expenditures have been even larger in Japan on a relative basis, but any sustaining

improvement in the economy has been elusive. The European Central Bank (ECB) is the latest to pursue

an aggressive QE program, its effectiveness has yet to be measured. Gold’s role as an alternative

currency is also that of an insurance policy.

As the numbers get larger, the stakes can become bigger as well as the ramifications for changes to

policies. The Swiss, who have a strong currency but have trying to keep a lid on that appreciation

relative to the Euro, last week unexpectedly reversed course after maintaining that relative peg in

currency values became too expensive. The surprise shift in policy resulted in an almost instantaneous

15% move in the relative value of the Swiss Franc to the Euro – a magnitude of change virtually unheard

of between major currencies. Events such as this reflect the growing influence central bank policies

have on markets and the volatility that can be unleashed as result of unexpected changes to those

policies. We believe a little insurance is a good thing for a portfolio in an environment where volatility

may trend higher.

Lowe Wealth Advisors is an SEC registered investment adviser that maintains a principal place of business in the State

of Maryland. The Firm may only transact business in those states in which it is notice filed or qualifies for

a corresponding exemption from such requirements. For information about the registration status and

business operations of Lowe Wealth Advisors, please consult the Firm’s Form ADV disclosure documents, the most

recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at

www.adviserinfo.sec.gov.

This commentary is intended for the dissemination of general information regarding market conditions

to Lowe Wealth Advisors clients. The information contained herein should not be construed as personalized investment

advice. Past performance is no guarantee of future results, and there is no guarantee that the views and

opinions expressed in this report will come to pass. While any general market information and statistical

data contained herein are based on sources believed to be reliable, we do not represent that it is

accurate and should not be relied on as such or be the basis for an investment decision. Any opinions

expressed are current only as of the time made and are subject to change without notice.