Bradley Williams, Lowe Wealth Advisors Chief Investment Officer

January 12, 2015

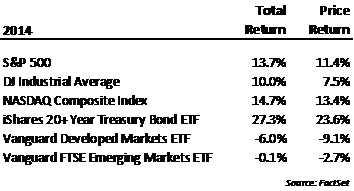

Despite international turmoil, mixed global economic data and the wind-down of the Fed’s quantitative easing program, the U.S. equity markets enjoyed another year of solid gains in 2014. The S&P 500 delivered a total return of 13.7% and marked its sixth consecutive annual gain – achieving that streak for the fourth time since 1928. By and large, the performance of the U.S. equity markets exceeded that of other markets around the world as returns reflected by the broad ETFs for developed markets and emerging markets both saw losses in 2014.

The consensus overwhelmingly looks for a repeat in 2015. In just one example, the December 23, 2014 issue of Barron’s includes a survey of Wall Street strategists who took a unanimously positive view of returns in the New Year. Of course, many times when there is a uniform consensus about the direction of a market it surprises everyone and does the opposite. That itself is not a downbeat forecast for equity market returns in 2015, but an observation of how markets often work. Look at the total return for long bonds in 2014 (see table of returns above). At the beginning of the year nearly anyone with an opinion thought rates were destined to go higher – but they didn’t. In fact they fell enough that the total return for long bond holdings exceeded that for equities in 2014.

Rather than add our own prediction of where the market might end up in 2015, we believe a more productive path is to review a few foreseeable factors that could influence the markets this year. This represents just a short list of events in which the outcome one way or another will impact markets, and unanticipated developments are almost certain to play a role in the direction of markets over the coming year.

One of the most important factors, in our opinion, continues to be the influence Federal Reserve policy has on the markets. In our prior quarter letter, we outlined the wind-down of the current quantitative easing program (QE3) and suggested this would coincide at the least with an increase in stock volatility. An update of the chart showing the S&P500 market behavior relative to the growth of the Fed’s balance sheet appears to reflect that increased volatility.

While the U.S. Fed is no longer providing direct quantitative easing to the market, investors continue to watch for subsequent changes in interest rate policy. Current expectations are for an increase in the short-term borrowing rate to occur at the April or June Fed meeting. The anticipated pace, comments and magnitude of subsequent actions will likely have a meaningful impact on our equity and fixed income markets. Faster and / or larger than expected increases without an acceleration in economic activity in the U.S. could present a more challenging backdrop for stocks.

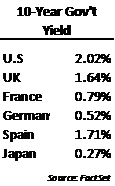

Alternatively, further accommodation, or slower or no movement on rates would likely extend the stimulative environment the market has thrived on for the past six years. If this sound impossible given the low absolute level(?) at which interest rates currently reside, consider the U.S. 10-year rate remains roughly 0.50% to 1.50% higher than the corresponding rates in Japan, Germany, UK, France and Spain, just to name a few. The Fed appears to have a monumental challenge ahead to balance the need to increase interest rates against the risk of hurting economic growth while the world is awash in ultra-low rates.

The policy decisions of the U.S. Fed are not the only central bank actions that investors will watch closely in 2015. The European Central Bank (ECB) convenes again on January 22. After it repeatedly intimated it is willing to do whatever it takes, the markets are now expecting a tangible plan of bond-buying stimulus to help counteract the languishing European economy. Action by the ECB could be received positively by major markets both inside and outside the European Union.

The European economy was the antithesis of our economy in 2014 as a steady deterioration increased the risk of recession again. The complexity of the European structure working within the single Euro currency complicates the task of delivering any economic stimulus, but the ECB has probably backed itself into providing further significant measures. Thus far, central bank stimulus actions around the world have been greeted warmly by the respective equity markets, but have been detrimental to the relative currency exchange rates. We believe either path – further stimulus or no response and additional economic weakening – will likely result in a continued decline in the value of the Euro relative to the U.S. dollar.

Aside from the actions and commentaries of central banks, the underlying economics still matter as well. In the U.S., trends in employment, consumer confidence and business spending intentions improved over the course of 2014 and generally outpaced the trends in other major global economies. Despite a weak start in the first quarter, U.S. economic activity expanded again in 2014 with GDP growth likely to finish around 2.2%, a similar level to 2013. Consensus expectations generally look for some acceleration in 2015 with many forecasts for U.S. GDP growth around 3.0%.

The economic recovery thus far has largely relied on consumer activity more so than business investment. Consumption is the largest component of the economy and consumers have contributed to that growth, leveraging the increased confidence that comes with an improved job outlook to make big purchases. This can be seen in auto sales, which rose to 16.4 million units in 2014 (the best since 2006) as the unemployment rate declined by a full percentage point during the year to 5.6%. However, moving economic growth beyond the low 2% range to 3% or more will likely require an increase in business investment to augment the trends in consumer spending.

Actual GDP growth in 2015 will ultimately be determined by many factors, but one we will continue to watch closely is the dramatic fall in the price of oil. Now down more than 50% from its high last summer, the magnitude of decline can cut economic fortunes both ways. Consumption surely stands to benefit from a redirection of spending and, according to a UBS study, could translate into a boost of 0.1% of GDP for every $10 decline in the price of a barrel of oil. However, a decline so steep that the prices fall below the cost of production risks stifling investment in that production and layoffs in the energy related businesses. The growth of oil production in the U.S. has been a significant contributor to the economic recovery over the past several years and fallout stemming from the price decline bears close monitoring.

Like it or not, the performance of many markets in 2015 is poised to be heavily influenced by the policies of central banks. We anticipate this will manifest itself in part through greater volatility for the U.S. stock market compared to the past two years. The trend in our economy remains constructive for the financial markets, but as we noted, there are many milestones that will bear evaluation, as well as inevitable unforeseen events. After six years of impressive gains in our equity markets, it is likely that we are in the second half of our economic expansion. Therefore, we want to be sensitive to more substantial changes in conditions if they arise. We remain focused on our objective of delivering compelling risk-adjusted returns for our clients over a complete market and economic cycle.

Lowe Wealth Advisors is an SEC registered investment adviser that maintains a principal place of business in the State of Maryland. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about the registration status and business operations of Lowe Wealth Advisors, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov.

This commentary is intended for the dissemination of general information regarding market conditions to Lowe Wealth Advisors clients. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results, and there is no guarantee that the views and opinions expressed in this report will come to pass. While any general market information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision. Any opinions expressed are current only as of the time made and are subject to change without notice.