No Thanksgiving Pardon for Oil

While markets here in the U.S. were closed for the Thanksgiving holiday, OPEC leaders were meeting in Vienna to discuss production cuts that could help offset the precipitous price decline oil has experienced since hitting an interim high in July. As is more often the case, however, the members of OPEC did not reach an agreement on quota reductions and the price of oil responded quickly, dropping more than 6% and falling into the $60s (oil was open for a shortened trading session on Thursday).1

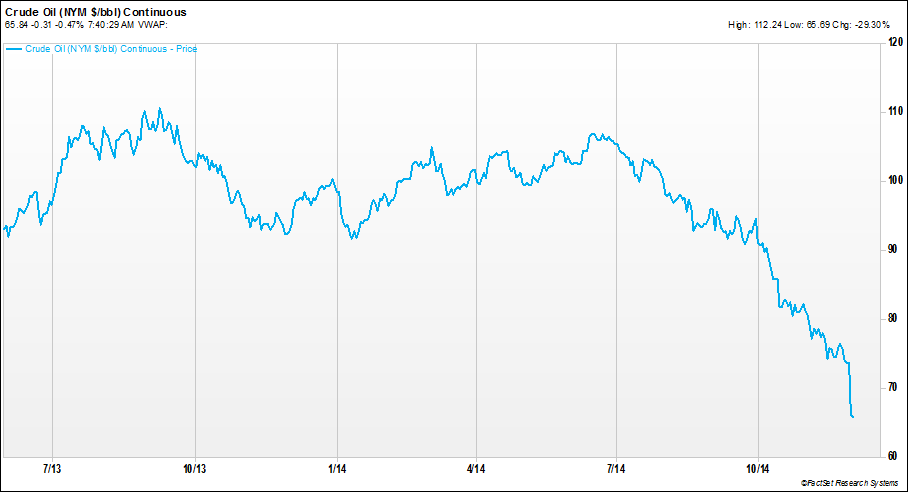

Follow-through weakness on the Friday after Thanksgiving now has West Texas Intermediate (WTI) oil trading at approximately $66 per barrel.1 This level represents a decline of almost 40% in just five months and begs the question how did we get here so fast and what does it mean for the investment landscape?

How or why we have seen such a marked decline in the price of oil over such a short period is difficult answer precisely. Whether it is geopolitical pressure being exerted on Russia or the Saudis putting pressure on U.S. shale producers or a result of economic weakness in Europe, the primary factor remains that the world is producing more oil than is currently being consumed and that results in lower prices.

More important is what this change in economics means for various world exporters and importers and the producers, particularly the fast growing shale oil companies here in the U.S. For countries that are net importers of oil and for consumers, the decline in the cost of energy is advantageous, lowering expenses and freeing up income for other spending. This should be nice tailwind for U.S. consumers, particularly as we move through the Holiday season.

Less excited about the sharp decline in oil prices are the domestic shale oil producers. Increased well efficiency and advanced drilling technology has enabled sharp increases in production in many regions of the U.S., but depending on the particular area, the price needed for these producers to breakeven can range from the low $50s to $90 or more per barrel.2 This means that the longer the oil prices stay well below $100, the more pressure on the cash flow of these companies and their ability to fund capital expenditures, pay dividends, buyback stock or service outstanding debt.

Stock prices for many energy related firms have already exhibited significant declines over the past four months, but one related asset class that has been slower to reflect potential risks is the high yield debt sector. Although spreads for high yield debt relative to investment grades have weakened some since late summer, we expect this trend could continue, or even accelerate, as energy companies have been active issuers of high yield debt. Energy companies represent approximately 15% of the high yield ETF that many Lowe Wealth Advisors clients hold..3 In our opinion, it is likely cash flow concerns will continue to weigh on the value of the debt for many of these issuers and could pose refinancing difficulties for some down the road.

1. Market price and return data from Factset Research Systems.

2. Wall Street Journal, Fracking Firms Get Tested by Oil’s Price Drop, October 9, 2014.

3. BlackRock iShares HYG fund data.

Lowe Wealth Advisors is an SEC registered investment adviser that maintains a principal place of business in the State of Maryland. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about the registration status and business operations of Lowe Wealth Advisors, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov.

This commentary is intended for the dissemination of general information regarding market conditions to Lowe Wealth Advisors clients. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results, and there is no guarantee that the views and opinions expressed in this report will come to pass. While any general market information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision. Any opinions expressed are current only as of the time made and are subject to change without notice.

• Not all portfolios are actively managed. If you have a question about how your account is being managed please contact us.

• No diversification can completely protect against market risk or other risk factors with investing. A diversified portfolio could still lose money.

• An Index is a portfolio of specific securities (common examples are S&P, DJIA, NASDAQ), the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Indexes are unmanaged portfolios and investors cannot invest directly in an index. Past performance is not indicative of future results.

• Foreign investing carries additional risk such as currency risk, political risk and different accounting standards.