Market Advance Continues

July 20, 2017

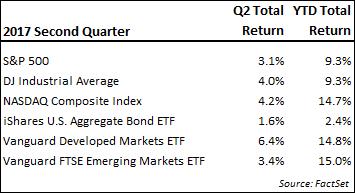

Equity markets advanced further in the second quarter, although not to the degree as in the first quarter. Gains were again rather broad-based as most asset classes and global regions saw appreciation. The most notable exception was the energy complex as oil declined more than 15% during the quarter. The S&P500 returned 3.1% during the quarter, while the tech-focused NASDAQ index gained 4.2%. Among international markets, the developed markets outperformed after years of lagging performance and exceeded the emerging markets’ gains over the course of the second quarter. The bond market was somewhat mixed, although mid- and longer-term maturities saw price gains as interest rates declined some from the first quarter.

Higher stock prices came despite a lack of progress on key deregulation and stimulative measures. Congress’ plans for healthcare reform, tax cuts, infrastructure spending and other deregulation initiatives were key in creating an expectation of economic growth and corporate earnings expansion. Those expectations have fallen steadily as political gridlock and distraction have made it less and less likely the hoped-for measures will pass. The legislative situation could change at any time, but if the trajectory of inaction continues, some expectations for higher growth and earnings factored in shortly after the election may need to be revised.

In the meantime, investor sentiment has been supported by continued progress in corporate earnings. Earnings for the first quarter (reported during the second quarter) were generally strong. The overall earnings growth rate for the S&P500 in the first quarter was 14%, the highest growth rate since the 16.7% seen in the third quarter of 2011. Corporate sectors including technology, healthcare, and financials were among the significant contributors, although the largest impact was from the energy sector. Earnings for the energy sector were near their lows in the early part of last year following the sharp decline in oil, and that made this year’s comparison in earnings growth for that sector appear much stronger than a trend. Overall, we believe corporate earnings continue to benefit from cost-cutting and low-interest rates, but revenue growth is below potential due to the ongoing tepid nature of the economic expansion. The 14% growth in earnings for the first quarter was an impressive figure to be sure, but we note it is not a growth rate that can be annualized.

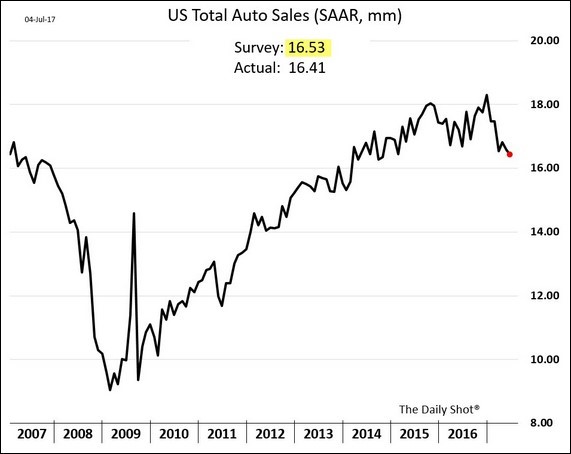

Aside from the stimulative contributions of the central banks, consumer spending has been one of the consistent sources driving this economic expansion. However, in our last quarterly letter, we noted that auto sales appeared to be seeing some exhaustion. The following chart of the monthly annualized vehicle selling rate shows the decline in activity off the recent peak despite the industry’s extensive efforts to extend sales growth. These efforts include chasing lower-quality buyers and offering more generous terms. According to Edmunds.com, the average loan length is now 69.3 months or nearly six years! As we noted in our last letter, we don’t view weakness in the auto industry as akin to the weakness in the housing sector in the early 2000s, but it is a window into one of the largest segments of the U.S. economy: consumer spending.

Beyond auto sales, consumer spending more broadly was somewhat disappointing in the second quarter. March retail sales reported in April were essentially flat and by the May report, we saw a contraction in activity. Sales were weak across a broad range of reported segments, although particularly so in consumer electronics and appliances. Faced with customers’ continued move to online shopping and Amazon’s expansion into more categories, traditional retailers have found this to be an extremely difficult environment. We don’t foresee all traditional retailers going away, but we expect there will be more news of retailers who don’t make it and significant changes in the face of traditional malls and shopping centers.

The softness in consumer activity was not enough, however, to alter the Federal Reserve’s inclination to raise rates and possibly begin unwinding some of the massive financial stimulus provided since 2008. In June, the Fed increased its rate target by 0.25% for a second time this year and indicated that it would likely make a third increase by year end. Additionally, it stated that by the end of the year it would begin to reduce the $4.5 trillion in assets held on its balance sheet, most of which came by way of stimulus expansion. As the Fed has shifted its stance on rates and stimulus, so too have other policy makers around the world. Most of the other major central banks have publicly contemplated some degree of similar adjustment.

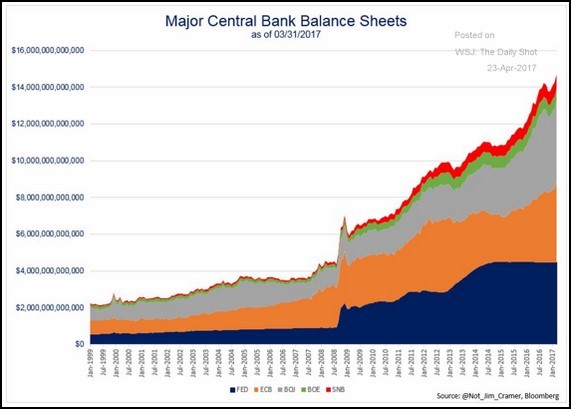

Arguably, the move away from ultra low rates is overdue, but it may now come at a time when there hasn’t been a meaningful acceleration in most of the economic factors that would typically accompany such a move. The degree to which our Fed or other central banks follow through on the reduction in stimulus remains to be seen, but we believe changes here could be very meaningful. The following chart shows the balance sheet expansion, or monetary stimulus, provided by the five major global central banks – U.S., Euro area, Japan, England, and Switzerland. The stimulus expansion since 2008 has coincided with the increase in many asset prices over the past decade and show that while aggressiveness of asset buying has shifted among the major central banks, the trend has remained remarkably consistent. We believe it is difficult to argue against at least some relationship between rising prices for stocks, bonds, real estate and other assets and the increase in global stimulus. Changes that may come in these policies should be watched closely.

The second quarter saw markets largely ignore the political turbulence in the U.S. in what continues to be a very complacent environment measured by asset price volatility. The outlook for corporate earnings has remained strong despite this policy uncertainty and some softness brewing among U.S. consumers. This may present some risk to future expectations. However, the most important factors for the market may very well come from changes in central bank policy. In our view, the flow of stimulus from central banks around the world has been powerful and overshadowed many factors that otherwise would have played a larger role in both market direction and valuation. That environment may be changing as our central bank and others around the world shift in posture. If, and how, these policy changes are implemented remains to be seen, but actions here could have a significant impact on future asset valuations and thus dictate more substantial shifts in portfolio allocations. As these developments unfold we will continue to communicate changes in our view and implications for client allocations.

An Aside on Bitcoin…

One asset class (if you can call it that) that saw an acceleration of momentum through the second quarter was that of the crypto-currencies, including Bitcoin. We have received several questions about Bitcoin as the gains for some of the various digital currencies during the past several months were truly breathtaking, even after substantial declines from peak levels hit in early June. We watch the prices of some of these “coins” as a means to measure sentiment and trading behaviors, but caution that these currencies carry with them tremendous amounts of risk. As an alternative currency, digital money, in theory, is supposed to represent scarcity and a store of value, but we have yet to see these currencies exhibit either of these qualities. While some forms, such as Bitcoin, have specified quantity caps, there is no limit on creating competing currencies. Some have equated the value of the currencies to the underlying blockchain technology, but we don’t think the “coin” value is representative of the transaction technology value. At this stage, we view crypto-currencies as an interesting market for observation, but in terms of investment see its risk qualities being on the spectrum with that of lottery tickets.

Bradley Williams, Chief Investment Officer

Lowe Wealth Advisors

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Lowe Wealth Advisors, LLC), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Lowe Wealth Advisors, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Lowe Wealth Advisors, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Lowe Wealth Advisors, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are a Lowe Wealth Advisors, LLC client, please remember to contact Lowe Wealth Advisors, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.