Relentlessly Higher

October 20, 2017

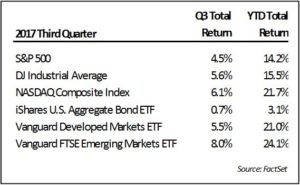

Equity markets saw broad-based gains in the third quarter in spite of natural disasters, threats of war, fiscal concerns (such as the debt ceiling debate) and more political turmoil. Healthy stock gains were seen in the U.S. markets and in most international markets. The S&P 500 returned 4.5%, the Dow Jones Industrial Average returned 5.6% and the technology-focused NASDAQ index saw a total return of 6.1% (Source: FactSet). The positive performance of the S&P 500 marked the eighth quarter in a row of gains for that index. International markets again outpaced the S&P 500 with emerging markets enjoying a total return of 8.0% in the quarter versus a 5.5% total return from developed foreign markets.

The bond market saw little net change over the quarter despite the Fed outlining a plan to begin reducing its balance sheet securities holdings and providing a strong indication it will raise rates again later this year. Interest rates, and therefore the bond market, fluctuated during this time, but by the end of the third quarter, the yield on the 10-year U.S. Treasury was within five basis points of where it began.

The gains in stocks, while impressive, are overshadowed by the relentless, almost methodical nature of the advance this year in the indices. The market gains during the quarter, and for the whole year, have not come as sharp bursts of activity like they did following the election. Rather they have been a product of almost daily small ticks higher. Merely characterizing this as atypical for stock market behavior glosses over just how unusual the performance has been. Below are a few statistics which demonstrate just how notable the current environment is.

Market Statistics of Note

- No decline greater than 3% this year, most benign environment in over 100 years (@michaelbatnick)

- Volatility Index (VIX) trades below 9 in third quarter, lowest reading ever (CNBC)

- Eight total daily moves in S&P 500 of more than 1%, least since 1965 (LPL Financial)

- Sentiment measures show optimism on par with or above levels last seen in 2008 (Market Vane, Wells Fargo/Gallup)

- Valuation measures at or near record levels with several past 1929 or 2000 levels (Price / Sales, Market Cap / GDP, Schiller Price / Earnings)

It’s difficult to point to a single reason why markets have become so unflappable, but it likely comes down to two primary factors – world financial markets continue to benefit from a large amount of monetary stimulus while the economic signals in major markets are not flashing warning signs. We have noted several times in the past the immense amount of financial stimulus central banks have been injecting into markets, but it is important to remember that even as the U.S. central bank ceased their stimulus program in late 2015, other central banks have continued to enact aggressive programs.

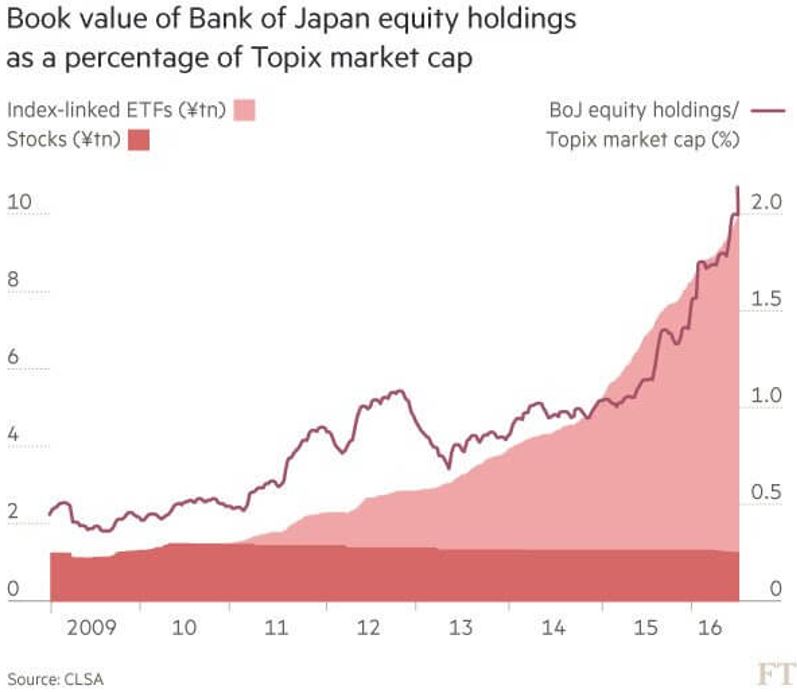

Based on calculations from Bank of America, year-to-date global financial markets have seen another $2 trillion in liquidity additions. Further, equity markets here and abroad have benefited directly from this stimulus as some central banks make purchases of stocks and exchange-traded funds (ETFs) an overt part of their policy. Examples include the central bank of Israel, which in 2016 moved to invest 10% of foreign reserves in foreign equities (Haaretz), the Swiss central bank, which has around $80 billion in U.S. stock holdings (Forbes), and the Japanese central bank, which has been so prolific (see chart) they have become one of the most influential forces in the world’s fourth-largest equity market.

In September, the U.S. Fed outlined its plan to begin reducing its stimulus program in October by not reinvesting a portion of the maturing securities held in its account. The initial plan is for a reduction of $300 billion over the next 12 months, which appears to be a lot of money, but actually, represents less than 10% of the $4.5 trillion of securities held by the Fed. Still, small changes in policy can sometimes have a big effect, and we think markets have become quite accustomed to the one-way nature of the stimulus. We will be watching closely for changes in the market environment following this shift in policy and whether the change at the U.S. Fed prompts adjustments by other central banks. Ironically, too much success in the early curtailment of the stimulus could embolden stronger action and tightening actions by other central banks. In our opinion, this bears close scrutiny as tightening actions by central banks have frequently marked the end of bull markets.

One of the reasons the Fed may be more inclined to finally reduce accommodation is that the world has moved into a position where all major economies are seeing some level of expansion. Rates of growth remain tepid in several major markets, but for the first time since 2007, all 45 major countries tracked by the OECD (Organisation for Economic Co-operation and Development) are expected to see growth this year (Wall Street Journal). The synchronized growth outlook provides a favorable backdrop for corporate earnings and generally makes investors inclined to focus more on growth and less on managing risk exposure.

Synchronized growth is an enviable position. However, we don’t believe it necessarily translates into an opportune time to strive for higher returns or set aside attention to portfolio risks. The broad growth environment is not a signal itself that the bull market is over, but it likely implies the cycle has become prolonged. As noted, the last time the world was in this position was 2007, just a year before things started to roll over for the U.S. economy and other foreign markets — not a good time to increase risk exposure. In the meantime, the lack of global economic headwinds creates no sense of urgency for investors and is likely a primary factor in the degree of complacency reflected in many market statistics such as volatility and interest rate spreads.

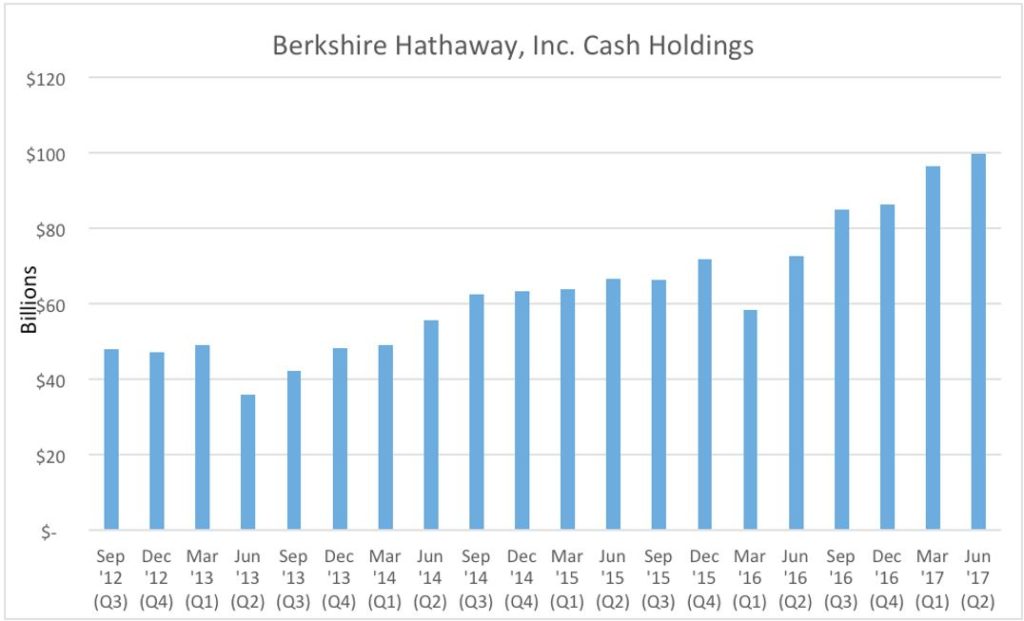

As we survey the landscape, we see the benign growth outlook generally offset by stretched valuations resulting in meager risk premiums for investors. In our opinion, the combination results in a much-reduced set of attractive investment opportunities and increases the importance of disciplined risk management. Interestingly, we note that other investors may be seeing a “strong” market, but facing similar difficulty in carefully investing capital. The graph below likely reflects that even Warren Buffett’s Berkshire Hathaway is seeing fewer opportunities as it has built up its largest cash holdings ever, despite low-interest rates.

Discussion of central bank policies on the market has become repetitive, but we believe necessary because of the extreme influence these actions have had on the current market cycle. We may now be entering a time when the nature of those policies begins to shift. Because of the duration of this market cycle and the extremes in factors like stock valuation and low-interest rates, managing a contraction of stimulus without disrupting economic growth could prove challenging. Tighten too quickly and growth could falter; too much stimulus or a reversal of policy and investors could lose confidence. We don’t know how the scenarios will evolve but will be closely watching the market response to changes in policy. As these developments unfold we will continue to communicate any changes in our view and corresponding implications for client allocations.

Bradley Williams, Chief Investment Officer

Lowe Wealth Advisors

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Lowe Wealth Advisors, LLC), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Lowe Wealth Advisors, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Lowe Wealth Advisors, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Lowe Wealth Advisors, LLC’s current written disclosure statement discussing our advisory services and fees is available upon request. If you are a Lowe Wealth Advisors, LLC client, please remember to contact Lowe Wealth Advisors, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services.